How do higher interest rates affect US stocks?

As the risk of sustained high tariffs on imports to the US receded in recent weeks, investors have turned their attention to another potential area of concern for the US stock market: rising interest rates.

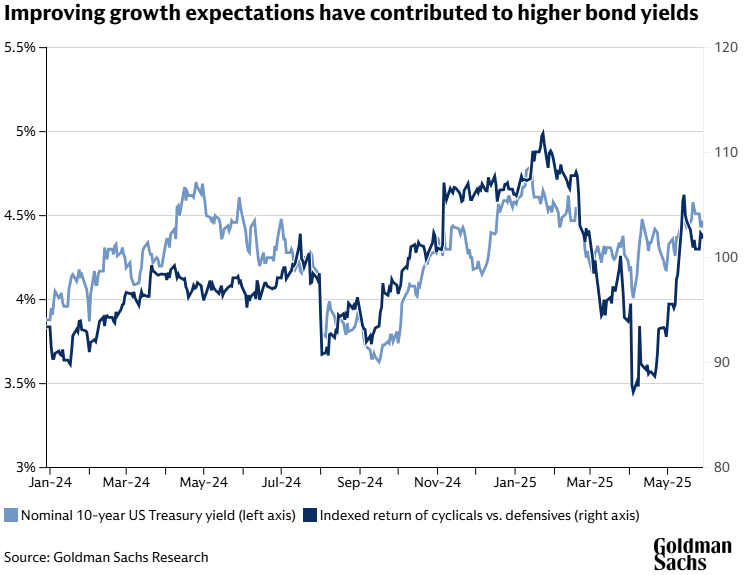

Several factors including a declining risk of recession, concerns about the path of US government debt, and higher borrowing costs around the world have contributed to an increase in US bond yields, according to Goldman Sachs Research.

Rising interest rates have the potential to impact stocks in several ways, including limiting the scope of potential growth for stock valuations and reducing company earnings.

The levels of bond yields themselves are not as important for stocks as the factors that are affecting interest rates, Goldman Sachs Research chief US equity strategist David Kostin writes in the team’s report. “Equities typically appreciate alongside rising bond yields when the market is raising its expectations for economic growth but struggle when yields rise due to other drivers, like fiscal concerns.”

Why are US bond yields rising?

The nominal yield on 10-year US Treasury bonds rose by 40 basis points in May, to 4.4%. That’s up from about 3.6% in mid-September. “The increase in bond yields was initially driven by cooling trade tensions and reduced recession risk. In recent weeks, spillovers from an increase in global bond yields, especially in Japan, and renewed concerns about the US fiscal outlook have also contributed to higher bond yields,” Kostin writes.

These factors have had a particularly pronounced effect on the term premium — the compensation that borrowers pay investors for holding long-term rather than short-term bonds. Estimates of the 10-year term premium have risen to the highest level since 2014.

Based on a combination of slow (but not recessionary) economic growth and above-trend inflation, Goldman Sachs Research’s rates strategists expect bond yields will remain around current levels in 2025. They expect the Federal Reserve will conclude its interest rate-cutting cycle in June 2026, with its policy rate at 3.5-3.75%.

The US fiscal outlook has been a focus for investors, and they’re scrutinizing how much the ratio of US debt to GDP, which is currently around 100%, may climb depending on budget policy. In the context of elevated inflation and low perceived risk of recession, our rates strategists note the risk that bond yields move even higher, similar to the August-October 2023 period when 10-year yields reached 5%.

How will higher bond yields impact US stocks?

The vulnerability of stocks to rising interest rates depends on the reason yields are rising. When higher bond yields are accompanied by a large improvement in economic growth expectations, stocks typically rise.

In fact, an analysis of weekly returns during the last few years shows that the market’s pricing of economic growth has been around three times more important than term premium (the additional risk of holding an asset with a later maturity) when it comes to stock prices. “This relationship was demonstrated in April and early May as improving growth expectations lifted both stocks and yields,” Kostin writes in the report.

The speed of the move in bond yields also has an impact on stock prices. Stocks have historically struggled when yields rise by more than two standard deviations in a month. Today, a two-standard-deviation monthly move would be roughly 60 basis points, which would bring the nominal 10-year US Treasury yield to around 4.9% — similar to the levels in January this year.

“Many investors point to 5% nominal yields as a key tipping point for stocks, but we are less convinced,” writes Kostin in the team’s report. An analysis of annual S&P500 returns since 1940 based on interest rates shows that there has been no clear relationship between the two. Goldman Sachs Research estimates that S&P 500 returns over the next 12 months will be more than 10%, bringing the index to 6500.

Even so, bond yields remaining at their current level could constrain the future valuations of stocks. Goldman Sachs Research’s macro model suggests that a 100-basis-point change in real Treasury yields is associated with a roughly 7% change in S&P 500 forward price-to-earnings (P/E) multiple. The team’s model indicates that the S&P 500 currently trades close to fair value due to strong corporate fundamentals, especially among the largest stocks, and their baseline forecast assumes the P/E multiple will be roughly unchanged in 12 months.

Bond yields can also affect stock earnings, because higher interest rates mean that companies pay higher borrowing costs. But despite a significant rise in interest rates, effective borrowing costs for the S&P 500 have only modestly increased since the start of 2022, because 72% of S&P 500 debt carries a fixed rate lasting beyond 2028. Rising interest rates are also normally associated with higher earnings for financial stocks.

As a result, the team’s S&P 500 earnings-per-share model shows that the net impact of a 100-basis point increase in bond yields on EPS is roughly neutral.

However, elevated interest rates may pose a larger risk to the earnings of small-cap stocks, according to Goldman Sachs Research. These smaller firms also operate at lower margins than bigger companies, which means they have less of a financial cushion against higher interest payments.

“We expect continued economic growth and a Fed on hold will keep yields elevated, sustaining investor preference for companies with strong balance sheets that are insulated from the pressure of interest rates,” Kostin writes.

This article is being provided for educational purposes only. The information contained in this article does not constitute a recommendation from any Goldman Sachs entity to the recipient, and Goldman Sachs is not providing any financial, economic, legal, investment, accounting, or tax advice through this article or to its recipient. Neither Goldman Sachs nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the statements or any information contained in this article and any liability therefore (including in respect of direct, indirect, or consequential loss or damage) is expressly disclaimed.

Our signature newsletter with insights and analysis from across the firm

By submitting this information, you agree that the information you are providing is subject to Goldman Sachs’ privacy policy and Terms of Use. You consent to receive our newletter via email.