The Future of European Defense

- Jared Cohen, President of Global Affairs and Co-Head, Goldman Sachs Global InstituteContributors: Wilson Shirley, Vice President, and Dejana Saric, Associate

Introduction

Europe is facing what may be its greatest security challenges since the Cold War. Russia's full-scale invasion of Ukraine and Moscow’s broader revisionism are acute threats. The continent has experienced a prolonged period of slow economic growth. Its primary security guarantor, the US, is confronting competing priorities in Europe, in the Middle East, in the Indo-Pacific, and at home. And critical and emerging dual-use and defense technologies, including AI-enabled systems, are reshaping the future of defense, even as Europe lags both the US and China in innovation.

These challenges have driven renewed interest in Europe’s defense sector: Europe’s real defense spending from 2014 to 2024 increased annually by 3.9% in real terms and European defense stocks have repeatedly hit records in 2025. And at the 2025 NATO Summit in The Hague, Allies committed to invest 5% of their gross domestic product (GDP) annually on core defense requirements and defense- and security-related spending by 2035.

When it comes to Europe’s defense, investors, executives, and policymakers are asking related questions: What steps can Europe take to enhance its security? How quickly can Europe rearm? What are opportunities to scale production from the largest European defense companies, and how can startups play a greater role? How can European states boost their cooperation, and how should they engage with the US and commercial partners globally? What is desirable and achievable, for governments and industry alike?

We provide an overview of the headwinds facing Europe’s defense industry and the tailwinds that could power it forward. We offer three potential scenarios for the future of European defense that, with the right strategic approach, European leaders could achieve.

What are the biggest headwinds to European security?

Europe’s most acute security threat is Russia. But the challenges to European security and its defense industrial base are structural and predate the Russia-Ukraine war. Underinvestment, deindustrialization, overregulation, and political and economic fragmentation have all contributed to make the European defense industrial base too small, too slow, and too fragmented to meet the continent’s security needs.

Decades of underinvestment have eroded Europe’s defense production, creating gaps in its capabilities. If all EU member states had spent just 2% of their GDP on defense, the NATO standard, from 2006 until 2020, it would have resulted in approximately €1.1 trillion in additional defense spending, larger than the annual defense budget of the US. But underinvestment has resulted in significant defense gaps. The European Commission’s white paper on European Defense Readiness 2030 identified Europe’s main production deficiencies as air and missile defense; artillery systems; ammunition and missiles; drones and counter-drone systems; military mobility; AI; quantum; cyber, & electronic warfare; and strategic enablers and critical infrastructure protection. Meanwhile, Europe’s overall industrial capacity and market share in key sectors have been eroded by China’s economic policies, as China’s exports have moved up the value chain in sectors like automobiles and specialized machinery.

Europe’s defense industry is fragmented, inhibiting its scale. European states and companies are smaller than many of their global counterparts, limiting their capacity to produce at scale. National interests, regulations, and a lack of coordinated procurement mechanisms increase the incentives for domestic manufacturing over cross-border investments and cooperation. Even as European defense spending has risen, intra-European collaboration has often decreased.

Europe relies on the US defense industrial base, which is facing competing priorities. From 2020 – 2024, approximately 64% of the defense procurement of European NATO countries came from the US. The US defense and aerospace industry has consolidated from over 70 suppliers in the 1980s down to single digits in the 2000s, resulting in some cases in reduced competition and capacity, as well as closed production lines. The US Commission on the National Defense Strategy found severe challenges to the US defense industrial base in its July 2024 report.

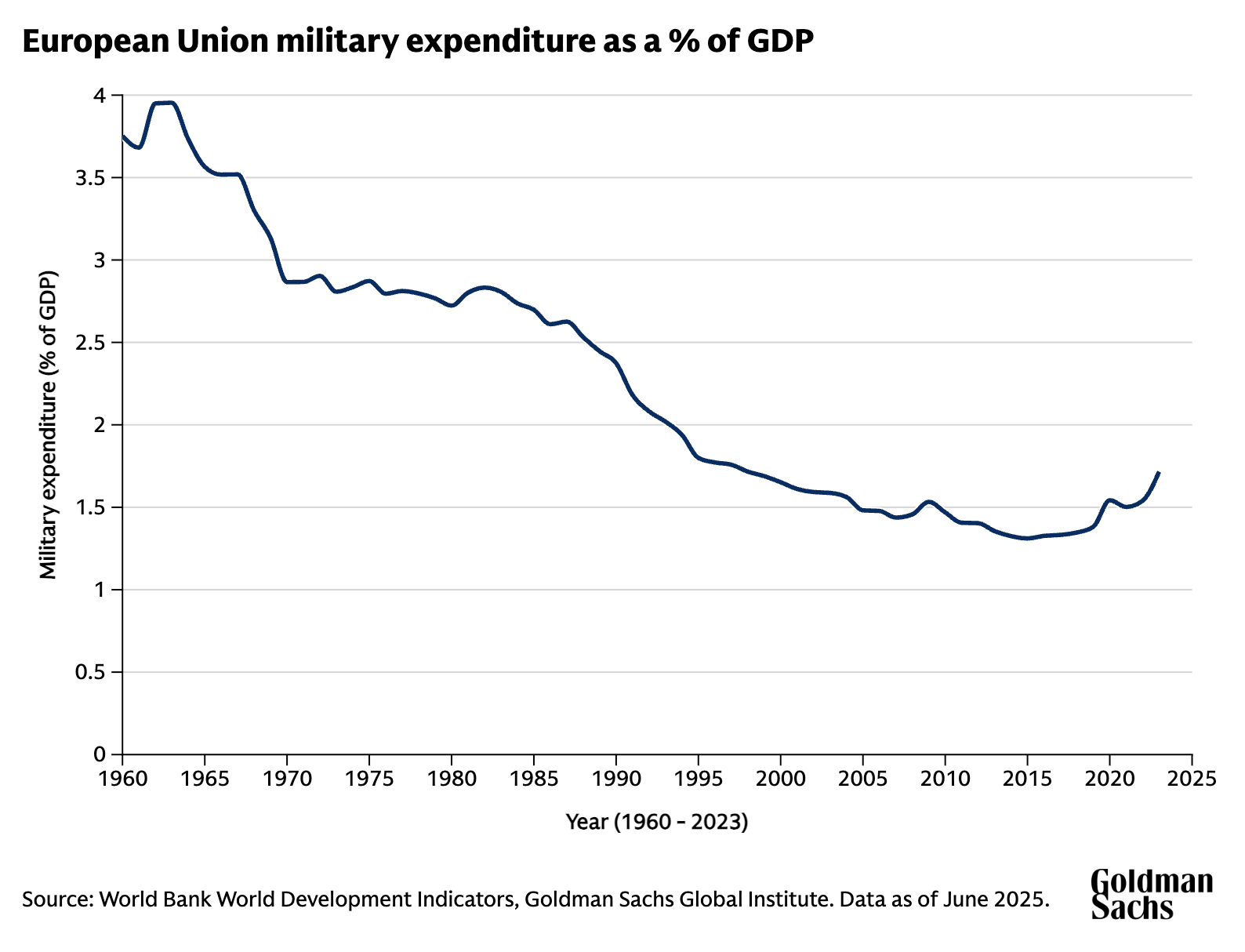

Europe’s slow economic growth has worsened its security challenges. In 2008, the eurozone’s GDP was $14.2 trillion, nearly equal to that of the US at the time. A decade and a half later, the eurozone’s GDP was $15 trillion, while that of the US has risen to $26.9 trillion. Even as defense investments as a percentage of GDP have increased markedly in many European countries, the relative size of European economies has declined, and so have their relative defense capabilities.

Regulatory barriers make Europe’s growth prospects worse, especially when it comes to the technological progress. Former Italian Prime Minister Mario Draghi’s report on European competitiveness observed that regulatory burdens on European companies impede innovation, especially for small and medium-sized enterprises and the digital sector.

Europe’s capital markets have less depth and liquidity than US capital markets, making it harder for companies to raise funds, innovate, and compete. Challenges to capital raising have impeded startup growth and innovation in Europe. As a result, European innovation in technologies has not scaled – only four of the world’s top 50 technology companies are European. The difficulty European companies often face in raising funds leads many to turn to deeper capital markets in the US, leaving a reduced pool of talent and projects to finance on the continent.

The EU is a monetary union, not a fiscal union. Europe is constrained in its ability to pool debt and coordinate large-scale, cross-border military investments across EU member states. The current EU budget amounts to €199.44 billion in total commitments, approximately 1% of EU GDP. Tight fiscal rules further limit debt and deficit levels. The European Commission is coordinating to allow member states to invest more in defense, but fiscal concerns remain, as do coordination challenges.

These connected challenges mean that revitalizing Europe’s defense industry could take many years—time it may not have. Developing advanced defense capabilities would likely require years of necessary investment and industrial buildup, a process that can be slowed by regulatory barriers within and between states. Coordinating investment and commercial activity across borders to fill capability gaps would require defense planning alignment at the national and multilateral level, by both industry and policymakers.

What are the tailwinds powering Europe’s defense industry?

Europe has significant advantages as a world power, including in the realm of foreign policy and defense. The European Union remains the world’s second-largest economy. Europe’s economic capacity, human capital, ongoing investments and reforms, and the leadership of Europeans at the national and supranational levels demonstrate that it can play a stronger role in global affairs. Europe’s current strategic challenges are a historic anomaly—within the memories of many European policymakers, the continent’s defense capabilities were stronger than they are today.

Europe has significantly more resources than its primary rival Russia. The EU’s combined GDP is more than nine times larger than that of Russia. At nearly 450 million inhabitants, the EU’s population is also approximately three times that of Russia.

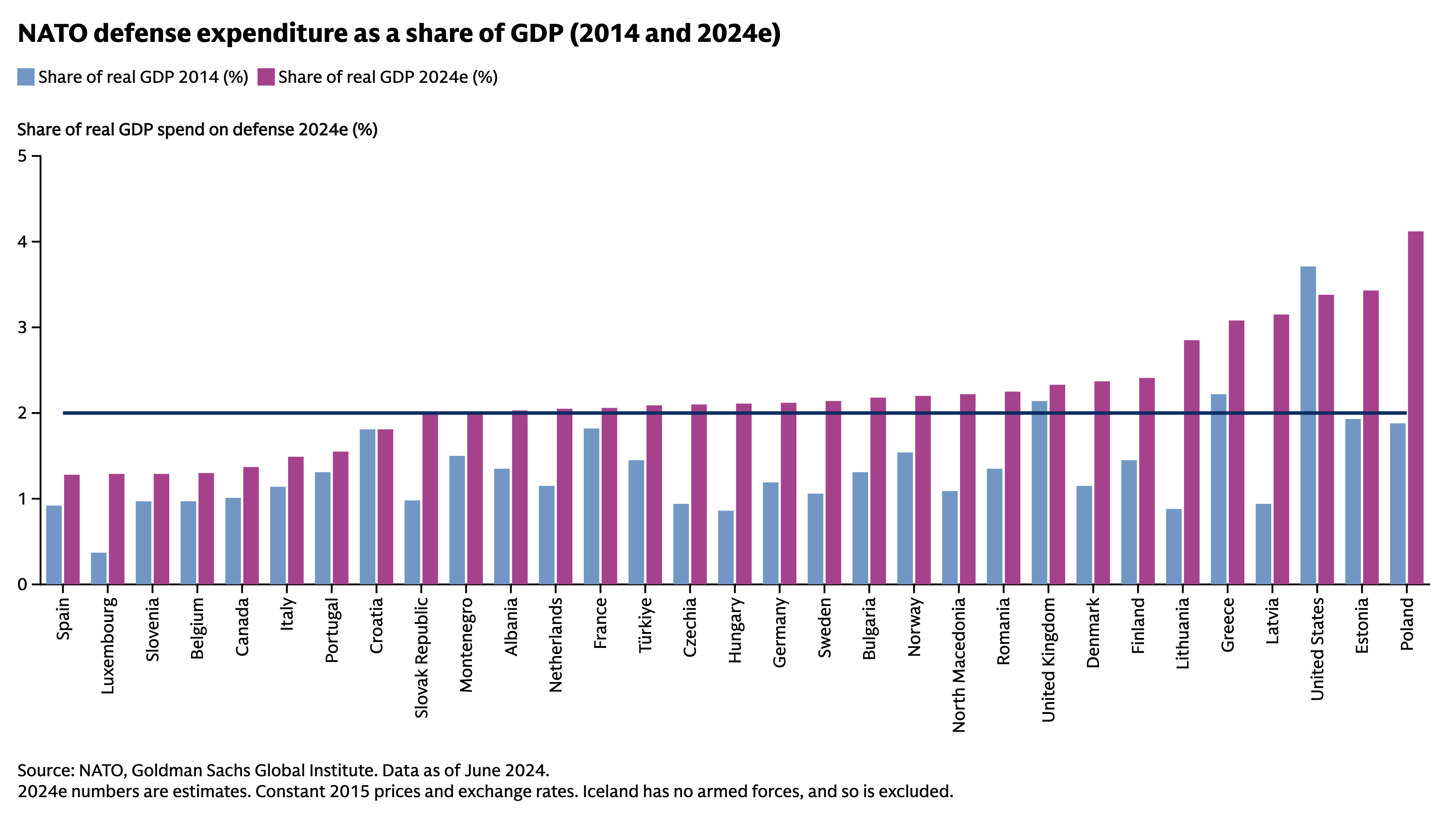

European NATO member states are increasing their defense investments. NATO member states, especially in Europe, have been increasing defense spending since at least 2014. Today, 23 of the 32 NATO members meet the 2% spending threshold agreed to at the 2014 NATO Wales Summit. At the 2025 NATO Summit in the Hague, member states agreed to a 5% target by 2035, including 1.5% for defense-related matters like cyber security and infrastructure.

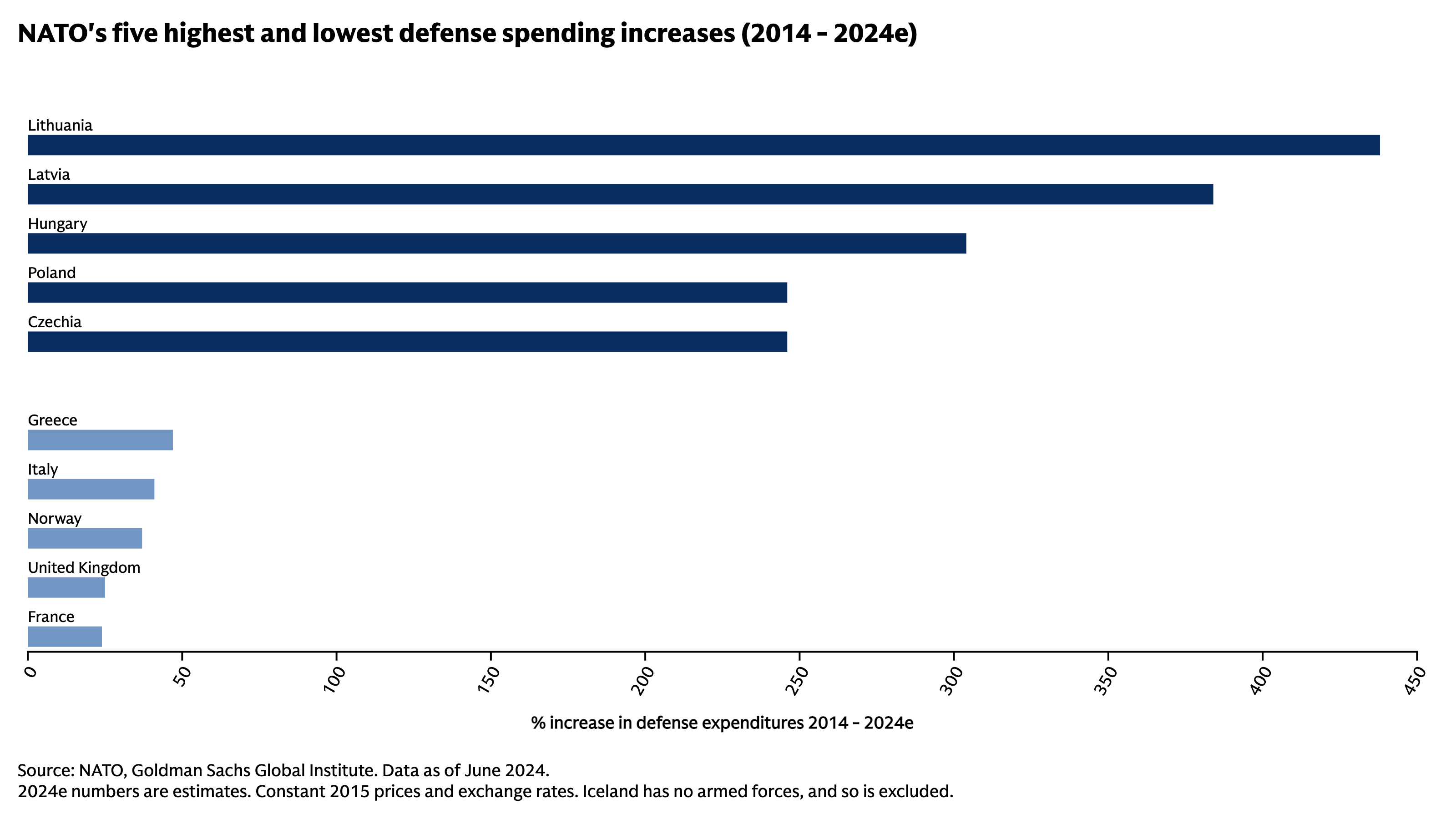

European nations are reforming their defense policies. In Germany, Chancellor Friedrich Merz has loosened limits on government borrowing, including the use of special funds to allocate defense investments free of a debt brake. The United Kingdom plans to add up to 12 attack submarines as part of the AUKUS program and, even before the 2025 NATO Summit in the Hague, was working to increase defense spending to 2.5% of GDP by 2027. Eastern European nations like Poland and the Baltic states are well above that total. Last year, 10 European NATO members increased their defense budgets by more than 20%.

The European defense industry is growing. European defense stocks surged as a result of renewed investments and pledges of more of a focus on defense. The continent is home to many world-class defense companies, many of which have increased production significantly since Russia’s invasion of Ukraine in 2022. Five of the 20 largest defense companies in the world are European (nine are American). Many of these defense companies have the capacity to ramp up production lines but have lacked the orders to justify such actions.

Europe provides substantial support for Ukraine, demonstrating the continent’s strategic capacity. The US has provided the most military support to Ukraine. However, Europe has provided most of the total international aid since February 2022. The EU and member states have made available over $158 billion in financial, military, humanitarian, and refugee assistance to Kyiv. Six European governments have invested more than 1% of their GDP in support for Ukraine. The European Commission’s financial and humanitarian aid comes to more than €50 billion.

The EU is acting. The European Commission’s ReArm Europe plan loosens fiscal rules to allow member states to spend an additional €650 billion on defense. More than half of member states intend to boost defense spending above the bloc’s spending limits. The Commission’s plan also includes a €150 billion loans-for-arms fund that will allow member states to procure weapons systems from European, and likely British, defense producers, with orders potentially coordinated by the Commission. The EU and the UK signed a new defense and security partnership in May 2025 that will formalize security cooperation.

Europe has enormous untapped economic and security capacities. Public investments, partnerships with the private sector, and competitiveness reforms, potentially along the lines suggested earlier last year by former Italian Prime Minister Mario Draghi can continue to move the needle.

What are the possible futures for European security?

Europe’s future defense posture and capabilities will be determined by the choices of its people and their leaders. Discussions of shoring up European capabilities have yielded wide-ranging proposals, from issuing European defense bonds to supporting joint borrowing, to establishing a rearmament bank, or even creating a “European Army.” Each of these may be unrealistic in the short and medium term.

While European leaders diverge on the best course of action to take, they are making reforms in at least three directions: 1) Investments in European-level security architectures, including those aimed at greater strategic autonomy, 2) the modernization of NATO, and 3) an agenda to boost European competitiveness and technological innovation.

Such courses of action can be pursued simultaneously. But they each involve tradeoffs.

Scenario #1: Greater strategic autonomy

European strategic autonomy, championed primarily by France, is the push to strengthen Europe’s ability to defend itself and reduce dependence on external powers, especially the US, for security.

The EU is already investing in Europe’s defense industrial base to strengthen its capabilities at home. The EU’s Security Action for Europe (SAFE) instrument is a €150 billion “loans for arms” program, and part of the European Commission’s ReArm Europe plan. SAFE creates preferential eligibility requirements for procurement from EU firms that would exclude or limit involvement from US enterprises. Likewise, the European Defense Fund aims to promote cooperation among EU defense companies, with approximately €5.3 billion of its nearly €7.3 billion budget allocated for collaborative capability development projects.

Additional EU-level economic reforms could boost Europe’s defense sector. The European Commission is developing a Defense Omnibus Simplification proposal to reduce regulatory barriers, ease access to financing, and facilitate cross-border collaboration. The Commission is also advocating for capital markets reforms to offer additional financing options and pathways to scale.

Long-term investments to revitalize European defense have yielded some progress. But strategic autonomy and a self-reliant European defense sector are unlikely in the short and medium term. Such changes would require sustained political commitments and cooperation among the EU’s 27 member states and their partners at levels we have not yet seen. Regulatory barriers, competition among members, and national commercial interests will likely slow progress. Meanwhile, Europe’s access to both legacy defense systems and critical and emerging technologies depends in large part on transatlantic commercial engagement. There is still no substitute for cooperation with the US and its defense ecosystem. Historically Europe has been strongest as a partner to, not a competitor with, the US.

Scenario #2: NATO modernization

NATO, despite differences among member states, is in many ways in a stronger position today than it was a decade ago. At 32 members, it is larger and has greater capabilities. A record 23 members are now spending 2% or more of their GDP on defense. The primary drivers of NATO defense spending increases are primarily central and Eastern European nations, while members in Western Europe and the Mediterranean have been slower to boost defense outlays.

The alliance is now focused on increasing defense investments, and on recognizing what other national assets matter for national security. The announcement of a new defense spending target of 5% by 2035, including 1.5% for defense-related spending, could scale this progress, ensuring that member states have more capable militaries and access to safe and reliable critical infrastructure, from airports, to rail lines, to cyber networks. Further European investments in NATO could strengthen the historic alliance and increase its members’ capacity for burden sharing.

NATO-first modernization would upgrade the alliance for the challenges of the era of Russian aggression, great-power competition, and technological disruption. Defense spending targets above the 2% threshold will further strengthen the alliance’s capabilities. Discipline and coordination in areas like procurement and investments, especially in research and development (R&D) for critical and emerging technologies, would modernize the alliance’s militaries and provide qualitative advantages. Early moves in this direction include NATO’s Innovation Fund and NATO’s defense innovation accelerator, DIANA.

Furthermore, NATO is working with global and regional coalitions to further enhance its capabilities and modernize its posture, given the challenges of global strategic competition. The alliance is collaborating with its Indo-Pacific partners, Australia, Japan, New Zealand, and South Korea, on support for Ukraine, cyber defense, and AI. The alliance’s capabilities have been boosted by the addition of highly capable members like Finland, which has adopted a comprehensive security model, a whole-of-society approach that augments its Defense Force of 280,000 active-duty and 900,000 reservists (in a country of roughly 5.5 million people). Meanwhile, regional groupings like the Joint Expeditionary Force, the United Kingdom-led, 10-nation Northern European military partnership, are taking on more prominence.

NATO remains the foremost security framework for many European countries and will likely continue to be the continent’s primary security guarantor. Greater regional and global defense cooperation could further boost the scale of Europe’s defense industries and overcome EU-level barriers to cross-border investment, trade, and capital flows.

Modernizing the NATO Alliance for today’s challenges is critical to the future of European defense. But modernizing the alliance is a generational task that would require overcoming political divisions, competing priorities and limited resources, and the perennial challenge of burden sharing.

Scenario #3: Techno-democratic partnerships

Artificial intelligence, autonomy, and industrial capacity are rapidly reshaping the character of war. But Europe lags behind the US and China in production and technological innovation, a fact that compounds its economic and security challenges. In the defense realm, key technologies include autonomous unmanned vehicles, cyber and space systems, and AI-enabled systems. Dual-use capabilities critical to modern defense are often invented, adopted, adapted, and produced at scale by the private sector.

With the right investments and alignments, a technologically-enabled industrial transformation could give Europe a chance to compete with, or even leapfrog, competitors and strengthen its security in the short term.

Europe’s defense technology sector is growing, driven in large part by commercial enterprises. From 2021 to 2024, investment into European defense technology startups increased 500% from the preceding three years. The NATO Innovation Fund (NIF), DIANA, and the European Defense Fund (EDF) have invested in Europe’s defense technology ecosystem as well. But compared to competitors, Europe’s defense technology sector is nascent for enterprises at all stages. Venture capital funding in Europe comes primarily from the US and Asia at late stages. Further investments in R&D, by the public and private sectors, can help close the gap, especially as Europe’s share of global R&D spending has fallen from 30.9% in 2000 to 20.5% in 2023.

Europe also has one of the world’s most advanced defense technology ecosystems on its doorstep: Ukraine. After more than three years of war, Ukrainians have mastered a rapid innovation cycle to adapt, test, and deploy dual-use technologies on the battlefield. Affordable first-person-view drones are produced at enormous scale of up to 5 million a year, and are now the most lethal equipment on the battlefield. Many of Ukraine’s drones use AI- and machine learning-enhanced systems to evade jamming systems, track targets, make predictions, and enhance decision-making. Additional private investments and government commitments can boost production capacity and further develop Ukraine and Europe’s AI capabilities.

The US defense technology sector is also an asset to Europe. Deeper integration with that ecosystem would strengthen transatlantic security and industry. The US is home to the world’s leading technology companies, especially in AI. And American defense technology companies have become significant global enterprises, offering cutting-edge defense hardware and software systems. The US has created models for public-private partnerships in the defense technology sector, including the Defense Innovation Unit (DIU) and the Office of Strategic Capital. Israel, the United Kingdom, and Turkey, each have robust defense innovation ecosystems as well, and are capable European technology partners.

Europe has two clear technologically powered paths to strengthen its defense technology ecosystem in the short term: The first is further engagement with transatlantic defense technology ecosystems, including integration between US and European commercial and research institutions. The second is support for and collaboration with Ukraine’s defense technology sector.

There is a critical window for this work today, as US defense production, including defense technologies, is scaling to meet increased demand. Meanwhile, Ukraine is contemplating lifting the export ban on its own defense industry. In turn, cooperation with US and Ukrainian defense technology enterprises could boost European defense primes and defense technology startups.

Technological innovation cannot solve all of Europe’s security challenges. The nature of warfare remains fixed, even as its character shifts. Legacy systems, including artillery and aircraft, remain central to modern warfare. But deepening defense technology cooperation is becoming a greater opportunity today, and a more urgent task, as Russia and its partners China, Iran, and North Korea are also learning lessons about the future of warfare from Ukraine, and deepening their own collaboration.

Conclusion

Europe faces a future where its competitive advantages could be further eroded, or where its investments made today can allow the continent to recover and modernize its historic sources of strength.

The latter path is not simple. In the last two decades, Europe’s structural economic, political, and innovation challenges have widened the gap between the continent and its partners and adversaries alike. Europe’s ability to overcome its security challenges, and to return to a path of greater economic growth, will depend on its capacity to invest in multiple priorities—in its own defense, in its historic alliances, and in critical and emerging technologies, including AI-enabled systems.

A stronger Europe would be a more powerful force in world affairs, aligned with the US-led security architectures, to deepen connections to transatlantic defense innovation, partner with Ukraine and other techno-democracies, and invest in its own capacity to compete across the board.

DISCLAIMER

The opinions and views expressed in this document do not necessarily reflect the views of Goldman Sachs or its affiliates. This document has been prepared by Goldman Sachs Global Institute and is not a product of Goldman Sachs Global Investment Research. This document for your information only and does not constitute a recommendation from any Goldman Sachs entity to the recipient. This document should not be copied, distributed, published, or reproduced, in whole or in part. This document does not purport to contain a comprehensive overview of Goldman Sachs’ products and offerings. This document should not be used as a basis for trading in the securities or loans of any companies named herein or for any other investment decision and does not constitute an offer to sell the securities or loans of the companies named herein or a solicitation of proxies or votes. Goldman Sachs is not providing any financial, economic, legal, investment, accounting, or tax advice through this document or to its recipient. Goldman Sachs has no obligation to provide any updates or changes to the information herein. Neither Goldman Sachs nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the statements or any information contained in this article and any liability therefore (including in respect of direct, indirect, or consequential loss or damage) is expressly disclaimed.

© 2025 Goldman Sachs. All rights reserved.

Subscribe to Briefings

Our weekly newsletter delivers the latest insights on economic forces shaping markets—from Goldman Sachs leaders, economists, and investors around the world.

You can unsubscribe at any time. For information about how your personal data will be used, visit Privacy Information and Resources.