What Is the US Economy’s Potential Growth Rate?

- US potential GDP growth is forecast by Goldman Sachs Research to average about 2.1% in 2025-2029 before accelerating in the early part of the next decade as AI boosts growth further.

- Our economists estimate that worker productivity has increased more quickly this decade: Labor productivity (outside the farm sector) grew 2% on average in the last five years, compared to about 1.5% pre-pandemic.

- Technology and related sectors like scientific research, engineering, and consulting have made significantly larger contributions to productivity growth than other sectors in the last five years. The tech industry’s increasing productivity is probably at least partially related to AI.

- Goldman Sachs Research forecasts that labor force growth’s contribution to potential GDP from will average about 0.3 percentage point over the next few years, which is lower than in recent decades.

Goldman Sachs Research expects the US economy to have a potential growth rate of more than 2% over the next few years, with some additional acceleration in the coming decade. Our economists anticipate artificial intelligence (AI) will increase labor productivity growth while workforce expansion slows.

The economy’s potential growth rate can be broken down into two key components: the contribution from growth in labor productivity (or real output per hour worked) and the contribution from changes in the size of the workforce, Goldman Sachs Research economist Manuel Abecasis writes in the team’s report.

What is the forecast for the US economy’s potential growth rate?

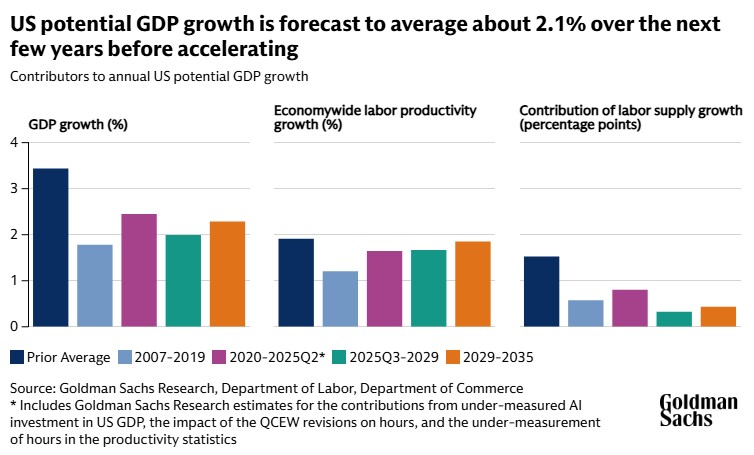

Goldman Sachs Research expects productivity growth across the US economy to increase 1.7% through 2029 and 1.9% in the early 2030s. Together with our economists’ forecasts for labor force growth, these estimates suggest that potential GDP growth will average about 2.1% in 2025-2029 before accelerating to 2.3% in the early 2030s as AI boosts growth further.

That’s a slightly lower potential GDP growth rate than the US is estimated to have had in recent years because elevated immigration boosted the size of the labor force, but it is well above the pre-pandemic pace. Since 2019, economywide labor productivity rose about 1.6% per year, well above its pre-pandemic average of 1.2%. At the same time, elevated immigration in 2022-2024 boosted annual labor-force growth to about 0.8% on average since 2019 (versus 0.6% before the pandemic). As a result, Goldman Sachs Research estimates that potential GDP growth rose from about 1.8% before the pandemic to around 2.4% in the years since.

What is the outlook for US economy’s productivity?

Our economists estimate that worker productivity has increased more quickly this decade: Labor productivity (outside the farm sector) grew 2% on average in the last five years, compared to about 1.5% pre-pandemic, according to Goldman Sachs Research. Growth in total factor productivity (economists think of TFP as technology innovation’s contribution to output) accounted for most of the acceleration. Nonfinancial corporate productivity growth was even stronger, at a 2.5% annualized rate since the fourth quarter of 2019 (after adjusting for some distortions).

“The bulk of the post-pandemic productivity outperformance has been driven by higher services productivity,” Abecasis writes.

Specifically, Goldman Sachs Research finds that tech and related sectors like scientific research, engineering, and consulting made significantly larger contributions to productivity growth in the last five years. These industries contributed about 0.3-0.4 percentage point of the overall acceleration in US productivity growth relative to its pre-pandemic pace.

The tech sector has been able to keep up a very fast pace of real GDP growth alongside sharply slowing employment growth over the last two years. Other high-value professional services sectors’ real GDP growth has strongly outperformed the pre-pandemic trend.

Could this reflect a productivity boost from AI?

“While it is probably premature to ascribe all of the acceleration to AI, these industries have some of the strongest use cases for AI technology, and we think the outperformance in tech productivity in particular is at least partially AI-related,” Abecasis writes. “In any case, the data suggest that the recent productivity rebound reflected a strong pace of technological innovation in sectors that are poised to benefit further from AI-driven improvements.”

Productivity gains from AI are expected to boost GDP significantly going forward.

“We also anticipate that frictional unemployment is likely to rise temporarily as AI adoption increases, in line with the experience of previous episodes of technological change,” he adds.

While the US economy’s potential growth rate will likely benefit from AI and other factors, it will also face some headwinds. Higher tariffs may be a drag on output and productivity over the longer run as they shift resources to less productive industries and weigh on investment. Deregulation and other investment incentives, on the other hand, will probably incentivize capital spending and improve efficiency.

How are changes in immigration impacting the US economy?

The other key component for an economy’s potential growth rate is the contribution from changes in the size of the labor force.

Before the pandemic, domestic labor force growth was on a gradually declining trend, largely reflecting slowing population growth amid declining fertility rates. An aging population put further downward pressure on labor force growth because older individuals have below-average participation rates in the workforce.

So far, however, the drag on labor supply growth from population aging has been smaller than feared because the labor force participation rates of older workers have increased.

Surging immigration from 2022-2024 led to a rapid expansion in the size of the labor force. But newly introduced, tighter immigration policy is likely to result in a slower pace of immigration that also slows the expansion of the workforce.

Taken together, the contribution of labor force growth to potential GDP growth is forecast to average about 0.3 percentage point over the next few years (versus 0.8 percentage point since 2019 and 0.6 percentage point in 2007-2019).

How AI and slower workforce growth will impact GDP growth

Goldman Sachs Research projects US economywide productivity growth to average about 1.7% through 2029 and 1.9% in the early 2030s. Together with its forecasts for labor force growth, potential GDP growth will likely average about 2.1% in 2025-2029 before accelerating to 2.3% in the early 2030s.

There are two main risks to Goldman Sachs Research’s forecasts, Abecasis writes.

“On the positive side, the main risks are that AI adoption happens faster than we expect or that current model breakthroughs eventually lead to artificial general intelligence,” he writes. “If this were to occur, potential AI innovation could lead to a large acceleration in productivity growth that eventually makes human input in knowledge-based work tasks redundant.”

“On the negative side, the main risks are that AI capex underperforms, population growth slows more abruptly than we expect, or scientific and technological progress slow down,” he adds.

This article is being provided for educational purposes only. The information contained in this article does not constitute a recommendation from any Goldman Sachs entity to the recipient, and Goldman Sachs is not providing any financial, economic, legal, investment, accounting, or tax advice through this article or to its recipient. Neither Goldman Sachs nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the statements or any information contained in this article and any liability therefore (including in respect of direct, indirect, or consequential loss or damage) is expressly disclaimed.

Our signature newsletter with insights and analysis from across the firm

By submitting this information, you agree that the information you are providing is subject to Goldman Sachs’ privacy policy and Terms of Use. You consent to receive our newletter via email.