2025 Annual Report

- The Goldman Sachs Group, Inc.Annual Report 2025

Letter to Shareholders

Fellow shareholders,

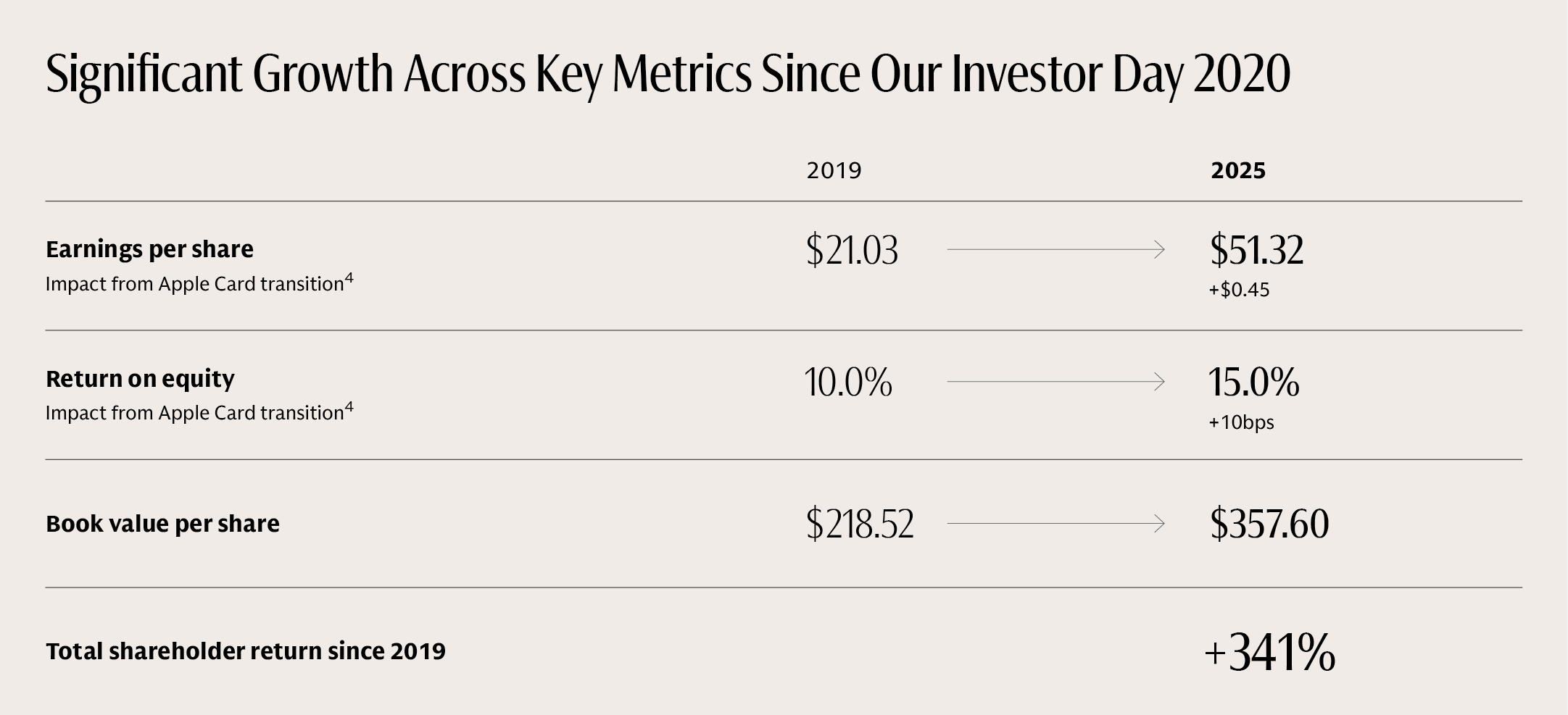

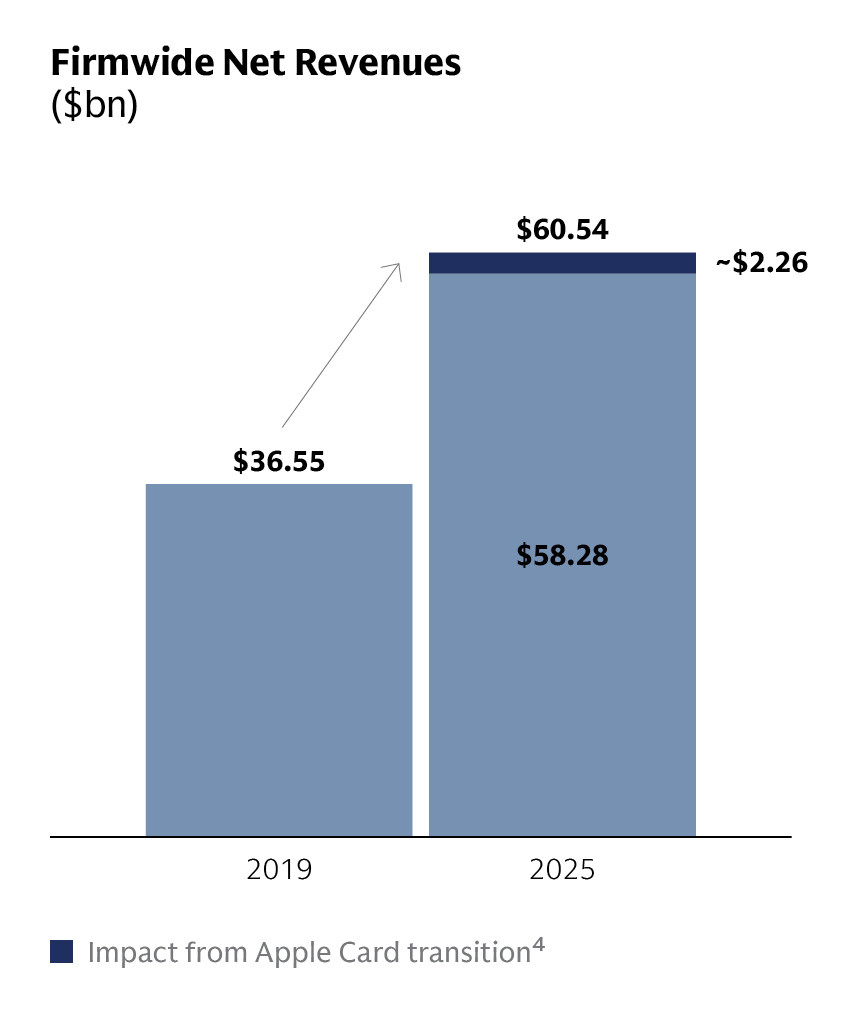

In a year marked by uncertainty and disruption, Goldman Sachs delivered strong performance across our world-class franchises as we continued to execute on our strategy and serve our clients with excellence. In 2025, we increased our net revenues year over year by 9 percent to $58.3 billion, grew our earnings per share by 27 percent to $51.32, and improved our return on equity (ROE) by 230 basis points to 15.0 percent.

When I look back on the past six years, I am proud of the progress we have made. At our Investor Day in January 2020, we laid out a clear strategy to grow and strengthen the firm and set several performance targets to hold ourselves accountable. Since then, we have increased firmwide net revenues by roughly 60 percent, grown earnings per share by 144 percent, improved our returns by 500 basis points, and delivered a total shareholder return of over 340 percent—the most of our peer group¹ over this timeframe.

At the same time, we have materially improved the risk profile of the firm and enhanced the resilience of our earnings. We have doubled our more durable revenues² and reduced historical principal investments³ by over 90 percent from roughly $64 billion to $6 billion. We saw the impact of our efforts to scale capital-light businesses and reduce our overall capital intensity in our most recent stress test by the Federal Reserve, with our stress capital buffer lowered by a cumulative 320 basis points since 2020.

This progress, coupled with the strength of our client franchise, positions us well for 2026. Our Global Banking & Markets (GBM) business is poised to capitalize on the upswing in strategic activity as well as the strong client flows across our FICC and Equities franchises. We see several clear growth opportunities in our Asset & Wealth Management (AWM) platform, including our liquid, alternatives, and private wealth businesses. In addition, the firm, overall, should benefit from a more balanced regulatory regime.

For all these reasons, we are confident in our ability to deliver on our through-the-cycle mid-teens return targets and, in the near term, exceed them—though I know our journey will not be a straight line. Conditions can change quickly, especially when policy uncertainty, geopolitical events, or technological developments cause market volatility. Even so, with solid momentum across our businesses, we are excited for the year ahead, as we continue to deliver for clients and drive attractive returns for shareholders.

Growing and Strengthening Our Core Businesses

Global Banking & Markets

In Global Banking & Markets, we maintained our position as the #1 M&A advisor⁵ in Investment banking for the 23rd year in a row. Very few—if any—service businesses of our size can claim long-standing leadership to this degree. This is a reflection of the strength of our client relationships, as well as the quality of our people and the advice and execution capabilities our people bring to our clients. Since 2020, we have generated an incremental $5 billion in advisory net revenues compared with the #2 competitor, and in 2025 alone, we advised on over $1.6 trillion of announced M&A transaction volumes, more than $250 billion ahead of our closest peer.

M&A transactions often catalyze additional activity across our entire franchise. Whether it is acquisition financing, hedging activity, or investing opportunities for our clients in AWM, the multiplier effect from our preeminent M&A franchise is powerful.

Another growth engine for GBM has been our leading origination and financing businesses. In 2025, we announced the creation of the Capital Solutions Group, which provides a comprehensive suite of financing, origination, structuring, and risk management offerings across public and private markets. In public markets, we are optimistic about Equity and Debt Underwriting, given the potential for a resurgent IPO market and acquisition-related financing activity. In private markets, our ability to structure holistic solutions through our uniquely strong origination and structuring has led to a number of asset-backed financings across infrastructure, transportation, and data centers. These types of transactions feed opportunities across our client franchise and our asset management platform.

FICC and Equities

In 2025, we maintained our position as the #1 Equities franchise alongside our leading position in FICC. ⁷ We have improved our standing with the top 150 clients ⁸ in these businesses, which, along with our strength in Investment banking, has contributed to 390 basis points of wallet share gains in GBM since 2019.⁹

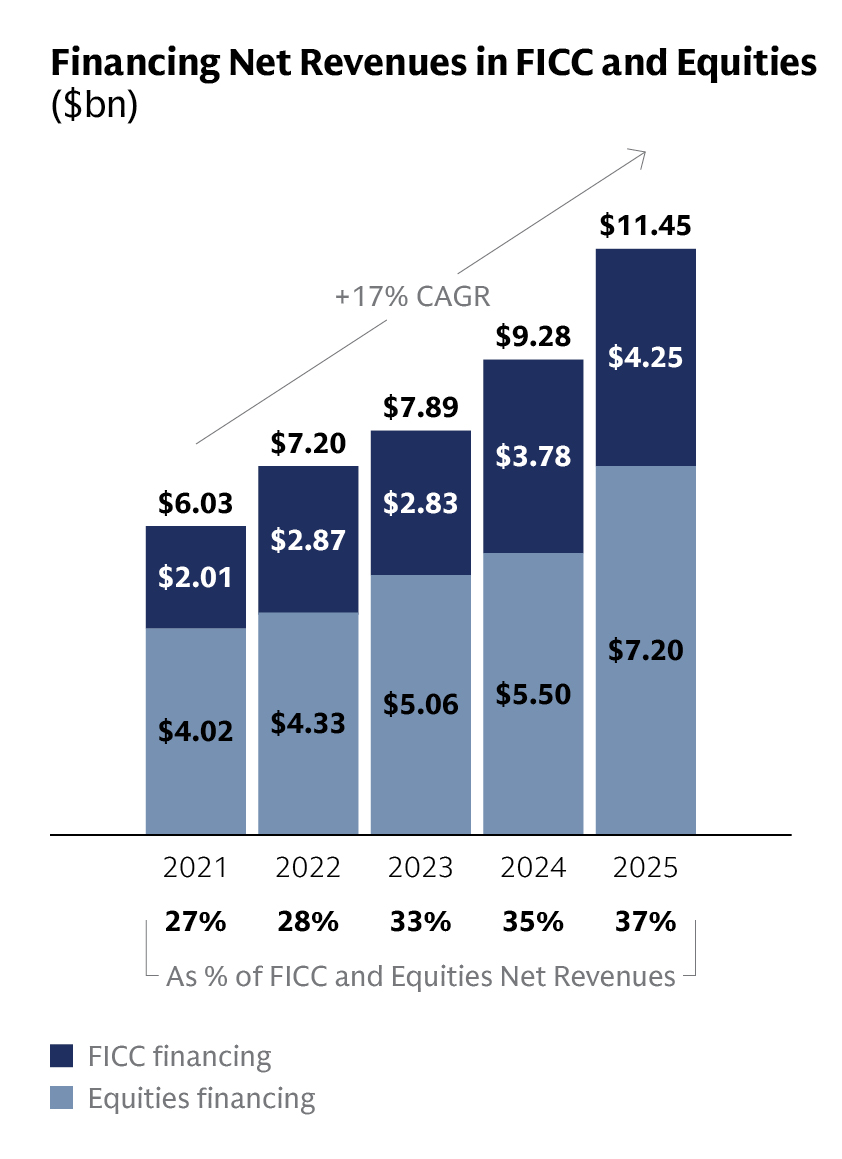

We also significantly increased our more durable FICC and Equities financing net revenues, which grew to a new record of $11.4 billion for the year. FICC and Equities financing provide secured and structured financing, securities lending, and portfolio solutions across FICC and equities markets to support our clients’ needs while at the same time providing a ballast to our results. In 2025, net revenues from these financing businesses were 37 percent of total FICC and Equities net revenues, and since 2021, they have increased at a 17 percent compounded annual growth rate (CAGR). With risk management always top of mind, we still expect to prudently drive growth from here.

"We have materially improved the risk profile of the firm and enhanced the resilience of our earnings."

In our FICC and Equities intermediation businesses, we have a demonstrated ability to deliver strong results in a broad array of market environments. While client activity levels in different asset classes ebb and flow in any given quarter, our overall results have been remarkably consistent over time. This reflects the breadth and diversification of these businesses, which have been bolstered by our share gains.

We see even more opportunities to strengthen our franchise. This includes investing to improve our market-making capabilities and broaden offerings for active and passive exchange-traded fund (ETF) issuers. In addition, we are working to close share gaps with key client segments including insurers, wealth managers, and registered investment advisors (RIAs), as well as in certain product areas like corporate derivatives. Geographically, we are looking to close the share gap in Asia, in part by focusing on these areas.

Asset & Wealth Management

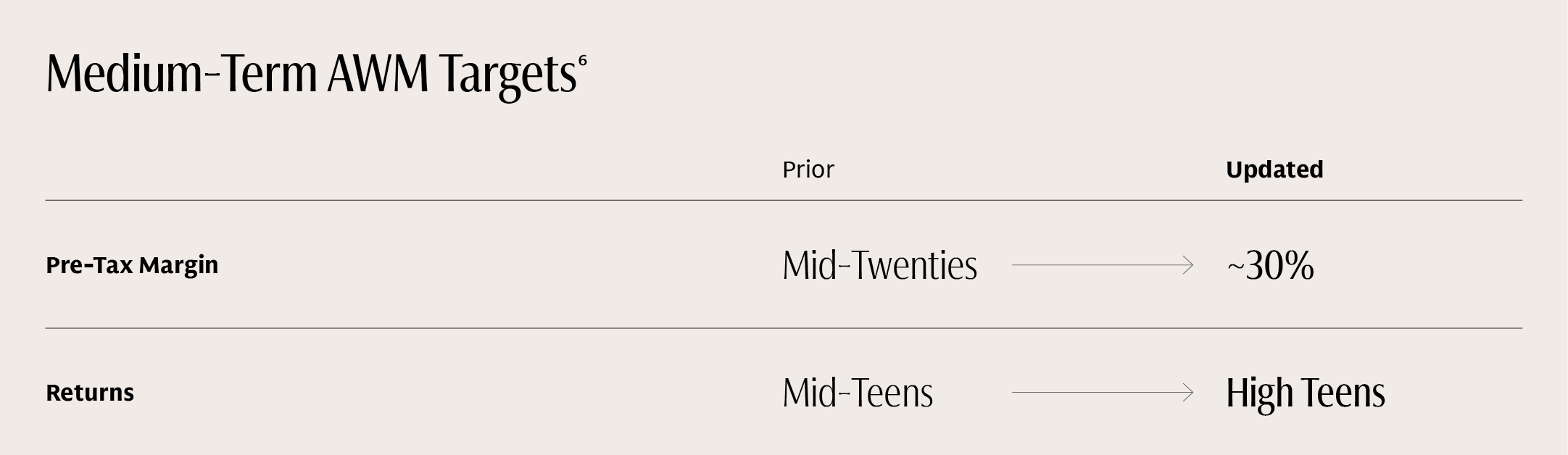

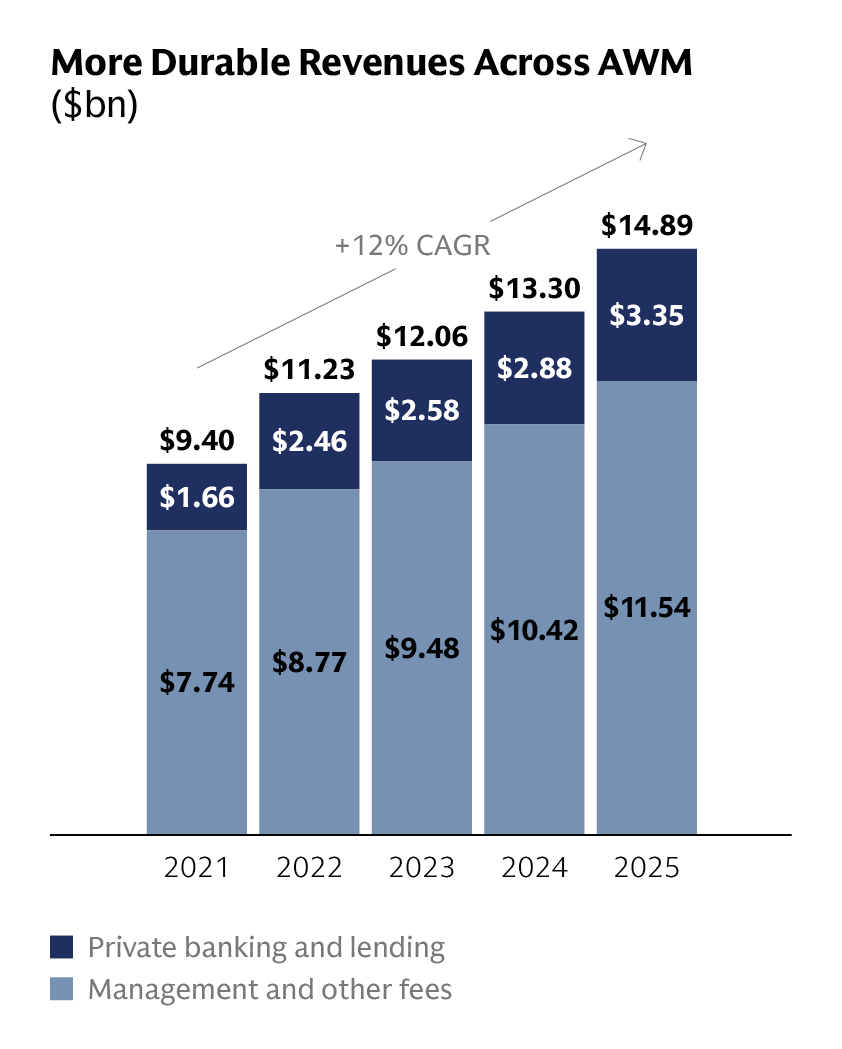

In Asset & Wealth Management, we are a top 5 global active asset manager,¹⁰ a leading alternatives franchise,¹⁰ and a premier ultra-high-net-worth wealth manager. Our scaled platform has $3.6 trillion in assets under supervision, with global breadth and depth across products and solutions. And, we have grown more durable revenues across Management and other fees and Private banking and lending at a 12 percent CAGR since 2021, exceeding our target. Given the improvement in our margins and returns, we have increased our pre-tax margin target to approximately 30 percent and our return target to the high teens.⁶ Going forward, we continue to see three key avenues for growth: Wealth management, Alternatives, and Solutions.

Growth Opportunities: Wealth, Alternatives, and Solutions

In Wealth management, we have built a premier franchise with $1.9 trillion in client assets¹¹ that is centered around meeting the distinct investing, planning, and borrowing needs of ultra-high-net-worth individuals, family offices, endowments, and foundations. Since 2021, we have grown Wealth management net revenues at a CAGR of 11 percent.

We expect further growth from here. Specifically, we are broadening our client base by increasing the number of advisors and content specialists globally. We are expanding our loan product and alternatives investment offerings. And, we are focused on elevating the overall client experience, including via enhanced digital offerings and more expansive thought leadership engagements that leverage the convening power of Goldman Sachs. To sharpen our focus on future growth in Wealth management, we have introduced a new target to achieve annual long-term fee-based net inflows of 5 percent of the channel’s long-term assets under supervision.

In Alternatives, we raised a record $115 billion in 2025 and have achieved $438 billion in gross third-party fundraising since our 2020 Investor Day. We continue to scale our flagship fund programs while concurrently developing new strategies that, together, produce strong performance for our clients. Given our success, we believe we can raise between $75 and $100 billion annually on a sustainable basis and generate double-digit percentage growth in Management and other fees from alternatives. We expect fee-paying alternative assets under supervision to reach $750 billion by the end of 2030.

In Solutions, we see secular growth in demand for our products and services. We are the #1 Outsourced CIO manager in the US,¹² the #1 separately managed account platform,¹³ and the second-largest insurance solutions provider.¹⁴ Looking ahead, we see continued opportunities for growth, including in third-party wealth in the context of alternatives offerings, ETFs, and customized solutions like direct indexing. In addition, we are expanding our capabilities in the retirement channel via partnerships, further deepening our strong relationships with insurers, and enhancing our offerings for institutional clients, including sovereign wealth funds.

“Goldman Sachs is well positioned in the year ahead to exceed our return targets in the near term, serve our clients with excellence, and create long-term value for our shareholders.”

Strategic partnership with T. Rowe Price and recent acquisitions

In 2025, we accelerated AWM’s growth trajectory with a strategic partnership and two announced acquisitions. We formed a collaboration with T. Rowe Price to deliver a range of public and private market solutions for retirement and wealth investors. In January 2026, we also acquired Industry Ventures, a venture capital platform that adds an attractive technology investment capability to our External Investing Group (XIG), which has over $500 billion in assets under supervision and is a market leader in secondaries investing.¹⁵ We also announced the acquisition of Innovator Capital Management, which will significantly scale our business to be in the top 10 of active ETF providers globally,¹⁶ particularly in the fast-growing outcome-based ETF segment. While the bar for M&A remains very high, we will continue to look for ways to accelerate growth in AWM.

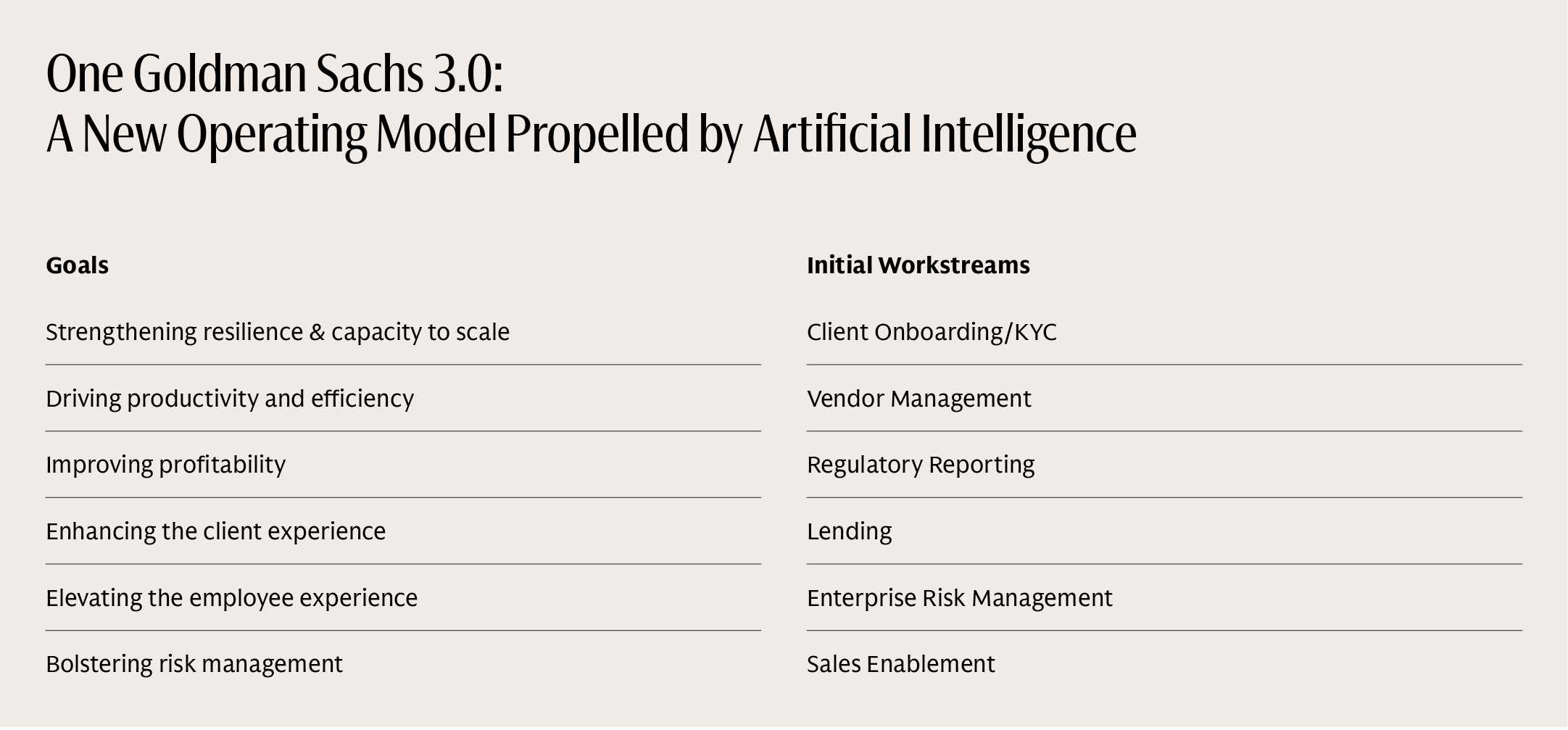

One Goldman Sachs 3.0

As an important component of our strategic priorities, we are focused on building a more modern, digital, and automated firm so we can continue to scale our operational capacity and effectiveness. In 2025, we announced the launch of One Goldman Sachs 3.0, our new operating model propelled by AI. The rapidly accelerating advancements in AI can unlock significant productivity gains for us, and we are confident we can re-invest those gains to continue delivering world-class solutions for our clients. It has become increasingly clear that our operating processes need to reflect the gains that will come from these transformational technologies.

To fully benefit from the promise of AI, we need greater speed and agility in all facets of our operations as well as the capacity to leverage timely, accurate, and complete data. This doesn’t just mean retooling our platforms. It means taking a front-to-back view of how we organize our people, make decisions, and think about productivity, efficiency, and resilience. In short, this is a moment for us to expand our One Goldman Sachs ethos to our internal operating model.

We are starting with six workstreams that we have identified as ripe for disruption: client onboarding/KYC, vendor management, regulatory reporting, lending, enterprise risk management, and sales enablement. Our teams are already seeing a number of opportunities in these areas to deliver the firm even more seamlessly to our clients and drive greater capacity for future growth.

Investing in Our People and Our Culture

Our greatest asset continues to be our people. Our client franchise is powered by our talent and culture—and it is critical that we continue to invest in them. Goldman Sachs is an aspirational brand, which allows us to attract quality talent at all levels. In 2025, we had over 1.1 million experienced hire applicants—a 33 percent increase from the prior year—and in our summer internship program, we maintained a selection rate of less than 1 percent.

Many of these individuals will have long careers at the firm, exemplified by the fact that nearly 45 percent of our partners started as campus hires, and while some leave for opportunities elsewhere, these firms often become important clients to Goldman Sachs. Today, more than 650 of our alumni are in C-suite roles at companies with either a market cap greater than $1 billion or assets under management greater than $5 billion.

The caliber of our alumni was on display last June when we held a dinner to mark 60 years since the establishment of our Management Committee in 1965. Among the 98 former and current members in attendance were three former secretaries of the Treasury, one current and one former governor of New Jersey, three former White House national economic advisors, and several current and former CEOs of large companies. It was special to see the easy rapport and camaraderie among such an extraordinary group of people, and it drove home the importance of preserving and enhancing our partnership culture well into the future.

“In this rapidly evolving environment, we remain focused on disciplined execution, investing for growth, and prudent risk management.”

Looking Ahead

In 2026, while it is difficult to predict the broader economic effects of the military action by the US and Israel against Iran, we still see the potential for a more constructive operating environment, based on a confluence of factors: fiscal stimulus in developed economies, monetary easing, AI capital investment, and a more balanced regulatory regime in the US. Put together, these are very powerful catalysts for people who own, transact, and invest in risk assets.

We also expect strategic activity to accelerate. Now that there has been a change in the regulatory environment, boards and CEOs feel there is a greater likelihood that they can execute on strategic transactions to expand their scale or improve their competitive position, and they are taking a much more front-footed approach. We expect this upswing to continue—though a protracted war or another exogenous event could, of course, change the current sentiment.

One of the key themes driving market sentiment is AI. On the one hand, we believe this technology is going to reshape the way we live and work, and the opportunity for productivity gains is extraordinary. But at the same time, there are significant questions as to how quickly this technology can be deployed and adopted. With any new technology, there will be winners and losers. In the early months of 2026, we have been thinking a lot about technology disruption, particularly amid the recent market volatility. While there are likely to be periods of recalibration, in the long run I believe the net benefits from AI will accrue to many institutions as AI investment continues to build.

Looking at the world more broadly, the geopolitical landscape continues to be complex, as seen over the last few weeks in the Middle East. In Europe, there has been much discussion about a proposal to form a savings and investments union, but so far progress has proved elusive. Until Europe’s 27 countries begin to act as an economic union, their geopolitical leverage will be limited, and the world will be worse off for it. I firmly believe a strong Europe is good for the world.

We also continue to watch closely the latest developments in the US–China relationship. After a period of heated rhetoric, both sides worked to de-escalate tensions in 2025. Now that the leaders of the world’s two largest economies are expected to meet multiple times face to face, we believe there is a roadmap for more meaningful dialogue. That said, it remains to be seen whether that dialogue will lead to a significant agreement. Given how entwined they are, it is important that the US and China reach a new modus vivendi, not just for the next 12 months, but rather for the next 10 to 20 years.

In this rapidly evolving environment, we remain focused on disciplined execution, investing for growth, and prudent risk management. In this last respect, we know from history that nothing is linear over time. While we remain optimistic about the operating environment, it is not hard to come up with scenarios where risks become a lot more pronounced. In recent weeks, for example, concerns about private credit, including underwriting quality or exposure to software companies that may be adversely affected by AI, are a reminder that the credit cycle has not been repealed. Higher levels of market volatility across various risk assets, elevated geopolitical uncertainty, and greater capital deployment, especially into AI, require diligent risk management. We view our ability to manage the risks we assume on behalf of our clients as our core responsibility and it is that responsibility that must be foremost in the minds of everyone at Goldman Sachs.

With our deep client relationships and a strong culture of risk management, we believe Goldman Sachs is well positioned in the year ahead to exceed our return targets in the near term, serve our clients with excellence, and create long-term value for our shareholders.

David Solomon

Chairman and Chief Executive Officer

Notes About the Letter to Shareholders

Forward-Looking Statements

This letter contains forward-looking statements, including statements about our financial targets, our business initiatives, and the use of AI and other productivity initiatives, including OneGS 3.0, our capital markets and M&A activity levels and the general operating environment, our completed and announced partnership and acquisitions, and the impact of potential changes to regulation and the regulatory environment. You should read the cautionary notes on forward-looking statements in our Form 10-K for the year ended December 31, 2025. For information about some of the risks and important factors that could affect the firm’s future results and the forward-looking statements, see “Risk Factors” in Part I, Item 1A of the firm’s Annual Report on Form 10-K for the year ended December 31, 2025.

1. Peer group includes MS, JPM, BAC, and C.

2. More durable revenues include FICC financing and Equities financing, within Global Banking & Markets, and Management and other fees and Private banking and lending, within Asset & Wealth Management.

3. Historical principal investments includes consolidated investment entities and other legacy investments the firm has exited or intends to exit over the medium term (three- to five-year time horizon from year-end 2022).

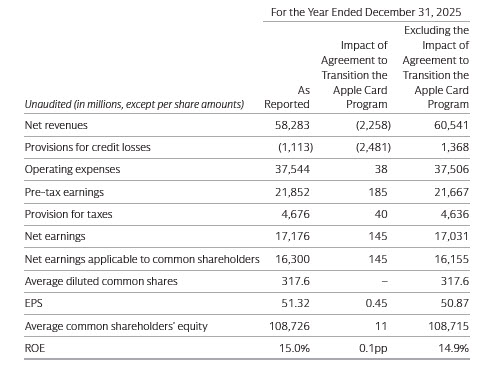

4. In the fourth quarter of 2025, the firm entered into an agreement to transition the Apple Card program to another issuer. Results reflect the impact of transferring the credit card portfolio to held for sale status and related impacts of contract termination obligations and other expenses. Management believes that presenting the firm’s results excluding these impacts is meaningful as excluding these impacts increases the comparability of period-to-period results. The firm’s results excluding these impacts are non-GAAP measures and may not be comparable to similar non-GAAP measures used by other companies. The table below presents the calculation of the firm’s results excluding the impact of entering into an agreement to transition the Apple Card program:

5. Ranking based on reported advisory net revenues (2003–2025).

6. Asset & Wealth Management pre-tax margin and return targets over the medium term (three- to five-year time horizon from year-end 2025). High-teens return refers to an ROE of approximately 17–19 percent.

7. FICC and Equities rankings based on cumulative publicly disclosed net revenues (2020–2025). Applicable peers are MS, JPM, BAC, C, BARC, DB, UBS, and CS (through FY22).

8. Top 150 client list and rankings compiled by GS through Client Ranking/Scoreboard/Feedback and/or Coalition Greenwich 1H25 (latest available) and FY19 Institutional Client Analytics ranking.

9. Global Banking & Markets revenue wallet share since Investor Day 2020 (2025 vs. 2019) based on reported revenues for Advisory, Equity underwriting, Debt underwriting, FICC, and Equities. Total wallet includes MS, JPM, BAC, C, BARC, DB, UBS, and CS (through FY22).

10. Global active asset manager and Alternative asset manager rankings based on assets as of 4Q25. Peer data compiled from publicly available company filings, earnings releases and supplements, and websites, as well as eVestment databases and Morningstar Direct. GS total alternative assets included assets under supervision for alternative assets and non-fee-earning alternative assets.

11. Consists of assets under supervision, brokerage assets, and Marcus deposits.

12. Rankings as of December 31, 2024. Source: Cerulli Associates; Largest OCIO Providers by US AUM.

13. Rankings as of June 30, 2025. Source: Cerulli Associates; The Cerulli Edge US Managed Accounts Edition 3Q25 (#97); Top-10 Managers: Manager-Traded SMAs.

14. Rankings as of December 31, 2024. Source: Insurance Investment Outsourcing Report; 2024 Insurance Asset Management Leaders.

15. Rankings based on 5-year trailing secondaries fundraising of managers (2020–2024) tracked by Secondaries Investor. Source: Secondaries Investor 2025 SI 50 Report, September 2025.

16. Active ETF providers ranking per Morningstar, as of December 31, 2025.

Subscribe to Briefings

Our weekly newsletter delivers the latest insights on economic forces shaping markets—from Goldman Sachs leaders, economists, and investors around the world.

You can unsubscribe at any time. For information about how your personal data will be used, visit Privacy Information and Resources.